Not Selling Hearing Aids and Its Effect on the Audiology Profession: A Comparison between Québec and Ontario

In the last few years the landscape of audiology has gone through tremendous changes in Canada and the US. Most notably, the marketing and dispensing of hearing aids has been the subject of ferocious debate. Active competition from “big box” companies such as Costco and the purchase of private clinics by hearing aid companies and/or consortiums have put enormous pressure on the shoulders of independent clinic owners to survive and expand.1,2 This has led to debate over the question of bundling versus unbundling the cost of clinician services with the selling price of the hearing aid.3–5 These events have even led to questions about the audiologist’s right to sell hearing aids—a right that was acquired through an American Speech-Language-Hearing Association (ASHA) initiative in the United State in the early 1970s.6,7 An intriguing question has emerged from all of the discussion: “What would audiology be like if audiologists would have never been granted the right to sell hearing aids?”

Although it’s impossible to go back in time, this question can still be partly answered by what could be called a case-control study. Indeed, there exist one province in Canada—Québec—where audiologists are not allowed to sell hearing aids. Indeed, a law amendment prohibits audiologists from selling hearing aids, as this act is restricted to the hearing aid dispensers only. A thorough search of the existing literature and an interview with a historian specialized in the health care professions did not provide a clear understanding of how this right became exclusive to hearing aid dealers (J Prud’homme personal communication March 25, 2015). Nonetheless, from the adoption of the law amendment in 1973 up to now, the act of selling hearing aids has been strictly restricted to hearing aid practitioners8 also called “audioprothésiste” in that province. Still, audiologists are allowed and trained to take ear impressions and to fit and adjust hearing aids. The present case-control study compares the profile of audiologists from Québec to audiologists from a neighbouring province, Ontario. These two provinces are similar in size, have similar populations (13 million vs. 8 million for Ontario and Québec, respectively) and both offer free universal health care programs.

Distribution of Audiologists by Sector

The general annual reports of both the colleges “Ordre des orthophonistes et des audiologistes du Québec (OOAQ)”9–14 and the “College of audiologists and speech-language pathologists of Ontario (CASLPO)”15–17 were analyzed in terms of the distribution of audiologists in the public versus the private sector from 2011 to 2016. The OOAQ annual report included the percentage of audiologists working within three areas of practice: public sector only, private sector only and public and private sector (audiologists working part-time in both sectors). The CASLPO annual report included only the percentage of membership by primary business setting for 2012, 2013, and 2014 (2011 didn’t include primary business settings and the 2015 and 2016 annual reports were not available at the time of the present article). For better comparison between Québec and Ontario, the primary business settings were categorized according to public versus private sector. Unfortunately, as the information provided by the reports was primary business setting only, estimation of mixed private and public employment was not possible with the current Ontario data.

To note, the number of audiologists is usually two times higher in Ontario compared to Québec (2011: 614 vs. 295, 2012: 620 vs. 321, 2013: 641 vs. 335, 2014: 665 vs. 369, and 2015: 724 vs. 402, respectively).10–17

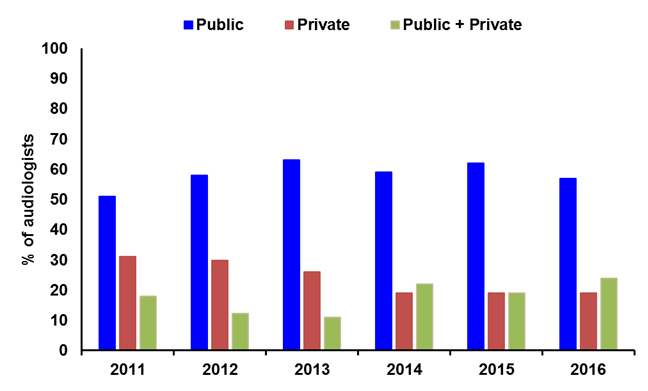

In Québec, the average percentage of audiologists working exclusively in the public sector was close to 60% over the last six years (see Figure 1). The public sector includes mostly hospitals and rehabilitation centres. When adding the percentage of audiologists with employment in both sectors (public and private) to the grand total, approximately 75% of audiologists in Québec depended on the public system for employment, either entirely or partly, over the last 6 years. This tendency was stable over the period of time between 2011 and 2016.

Figure 1. The percentage of audiologists in each sector in Québec.

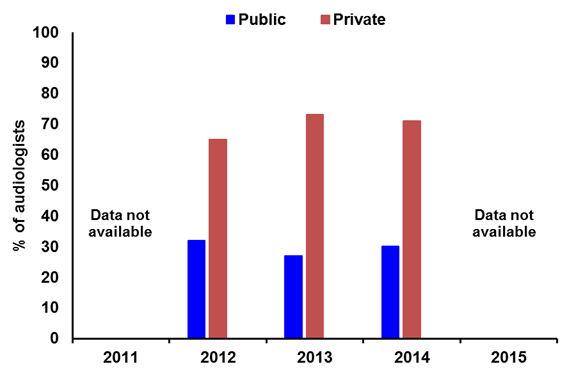

In Ontario, a completely different picture stands out: from 2012 to 2014, 70% of audiologists worked primarily in the private sector. The private sector includes private practices (independent owners and employees), health related business industries and group practice offices. Only less then a third (30%) of audiologists in Ontario worked in hospitals and rehabilitation centres (Figure 2).

Figure 2. The percentage of audiologists in each sector in Ontario.

Salaries of Audiologists and Other Health Care Professionals

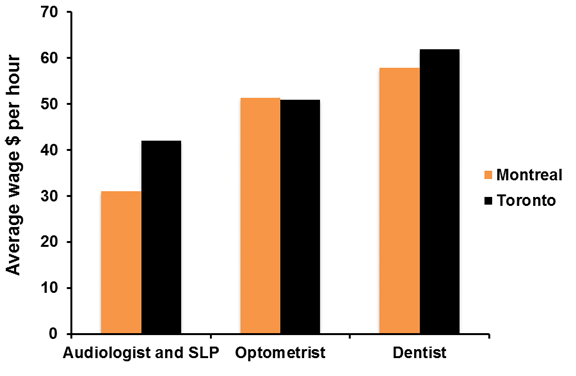

The average wage in dollars per hour was compared between professionals working in Montreal and Toronto, the two biggest cities in their own respective provinces. The three health care professionals that were included in the analysis were audiologists and speech-language pathologists (as one profession), optometrists and dentists. Dentists and optometrists were included in the analysis because they are health care professionals who are similar to audiologists in that they can sell products related to their field of practice. All data was extracted from the “livingin-canada.com” website.18–20 As mentioned on the website, the salaries for the audiologists and speech-language pathologists are representative of the years 2013, and salaries for the dentists and the optometrists are from 2011. Unfortunately, salary data was not available for audiologists and speech-language pathologists separately. Even Statistics Canada includes joint information about the two professions and does not separate them within their database.

As shown in Figure 3, there is a difference of 11.02 $/hour between the salary of audiologists and speech-language pathologists (SLPs) working in Toronto in comparison with those working in Montreal. This gap between Montreal and Toronto workers is non-existent for the optometrists which have a very similar salary of 51.3 $/h and 50.86 $/h, respectively. Finally, the salary of dentists in Montreal and Toronto exhibit a small gap of 4.03 $/h, in favour of dentists working in Toronto.

Figure 3. Average wage ($/hour) of audiologists and speech-language pathologists, optometrists, and dentists between Montreal and Toronto.

General Discussion

This comparison between Québec and Ontario in terms of the public versus private sectors and salaries has produced very interesting results. The first is the completely opposing distributions of audiologists by employment sector with Québec audiologists working mostly within the public sector and Ontario audiologists working mostly in the private sector. Although this difference cannot be attributed solely to the activity of selling hearing aids in Ontario and not in Québec, we can presume that this element is one of the most important. Indeed, the selling of the hearing aids is the primary source of revenue in most audiology clinics in Canada and the US.21 As this cannot be the case for audiologists in Québec, it can be presumed that most audiologists are not inclined to start businesses and clinics and invest their own money without hope of profitability. Most private practitioners in Québec are working in ENT clinics or hearing aid dispensers’ clinics, renting available equipment and performing hearing tests for ENT diagnosis or prior to hearing aid fitting by dispensers. There are only a handful of Québec audiologists who own their own clinics.

In the long term, this aspect could hinder the development of audiology services and thus affect hearing healthcare in Québec. Indeed, the increasing prevalence of hearing loss in the general population21,22 will likely result in a higher demand for audiology services.22 As almost 75% of audiologists are already relying solely or partly on the government budget for employment, one can presume that it will be difficult to meet the demand of hearing health care services considering tight government budgets resulting from a declining world economy. This situation is already a reality in Québec: to the knowledge of the Québec association of speech-language pathologists and audiologists (QASLPA), there haven’t been any audiologist positions created in hospital settings or in rehabilitation centres in the last few years. Most positions available in the public sector are non-permanent: either maternity leave replacements or contract positions. Graduating students are thus looking for positions either in the private sector or elsewhere in Canada or the wider world. As there hasn’t been any significant increase in the private sector from 2014 to 2016, one can speculate that graduating students are choosing mixed practice, leaving Québec, or changing professions.

Finally, the data provided also show a big discrepancy between the salaries of audiologists and speech-language pathologists working in Montreal and those working in Toronto, the two biggest cities in their respective provinces (Québec and Ontario, respectively). Unfortunately, the current data do not allow for salary analysis independently for audiologists and speech-language pathologists. The different organizations promoting those professions should advocate for the separation of information on speech-language pathologists and audiologists within federal agencies such as Statistics Canada. Still, the ~11$/h higher salary between speech-language pathologists and audiologists working in Ontario compared to Québec is the biggest one in comparison with optometrists (no difference) and dentists (~4$/h). Again, optometrists and dentists are both allowed in Québec and in Ontario to sell products related to their field of practice (e.g., glasses for optometrists, dental crowns for dentists), which could explain, at least partly, the biggest difference in salary between Montreal and Toronto for audiologists and SLPs.

In conclusion, the audiology profession is currently facing challenging times throughout the world, and the selling of hearing aids is often discussed in debates regarding the future of the profession. Lessons can be learned from the Québec experience, where audiologists are, uniquely in North America and probably in the world, not allowed to sell hearing aids. This, in turn, has probably led to insufficient development of private practices in that province and to lower salaries, at least compared to Ontario, a neighbouring province. While the public sector in that province is probably one of the most developed in the country, with several rehabilitation centres and hospitals including audiology services, one might wonder if the growth of the audiology public sector is sustainable considering government budget restrictions and priorities.

REFERENCES

- Granville B. Top-10 reasons why big box retailers have a love affair with hearing aids., Hear Rev 2015. Available at: http://www.hearingreview.com/2015/09/top-10-reasons-big-box-retailers-love-affair-hearing-aids/.

- Unknown Author. Hearing aid sales increase by 4.8% in 2014; RICs continue market domination. Hear Rev 2015. Available at: http://www.hearingreview.com/2015/01/hearing-aid-sales-increase-4-8-2014-rics-continue-market-domination/.

- Hamill TA Bundling versus unbundling. Aud Online 2002. Available at: http://www.audiologyonline.com/ask-the-experts/bundling-versus-unbundling-688.

- American Speech and Hearing Association. Unbundling hearing aid sales. 2016. Available at: http://www.asha.org/PRPSpecificTopic.aspx?folderid=8589934966§ion=Key_Issues.

- Protti-Patterson E. Private practice, bundling/unbundling, and CPT codes: Interview with Elizabeth Protti-Patterson, AuD. Am Acad Audiol Interv 2015. Available at: http://www.audiology.org/news/private-practice-bundlingunbundling-and-cpt-codes-interview-elizabeth-protti-patterson-aud.

- Staab W. History of hearing aid dispensing – V. Hear Health Tech Matters 2013. Available at: http://hearinghealthmatters.org/waynesworld/2013/history-of-hearing-aid-dispensing-vi/.

- Jacobson GP. James F. Jerger, PhD, responds to five questions. J Am Acad Audiol 2014;25(4):308.

- Office des professions du Québec. Chapitre C-26, Code des professions du Québec. 2016. Available at: http://legisquebec.gouv.qc.ca/fr/showdoc/cs/C-26.

- Ordre des orthophonistes et audiologistes du Québec. Rapport annuel 2010-2011, les membres, p.37; 2011.

- Ordre des orthophonistes et des audiologistes du Québec. Rapport annuel 2011-2012, ses membres, p.53; 2012.

- Ordre des orthophonistes et des audiologistes du Québec. Rapport annuel 2012-2013, ses membres, p.67; 2013.

- Ordre des orthophonistes et des audiologistes du Québec. Rapport annuel 2013-2014, ses membres, p.63; 2014.

- Ordre des orthophonistes et des audiologistes du Québec. Rapport annuel 2014-2015, ses membres, p.75; 2015.

- Ordre des orthophonistes et des audiologistes du Québec. Rapport annuel 2015-2016, ses membres, p.68; 2016.

- College of Speech-Language Pathologists and Audiologists of Ontario. Annual report, committee reports, p.6; 2012.

- College of Speech-Language Pathologists and Audiologists of Ontario. 2013 annual report, registration committee, p.16; 2013.

- College of Speech-Language Pathologists and Audiologists of Ontario. 2014 annual report, 2014 membership statistics’, p.19; 2014.

- Living in Canada. Audiologist and Speech-language Pathologist salary Canada. 2016. Available at: http://www.livingin-canada.com/salaries-for-audiologists-and-speech-language-pathologists.html.

- Living in Canada. Optometrist Salary Canada. 2016. Available at: http://www.livingin-canada.com/salaries-for-optometrists.html.

- Living in Canada. Dentist Salary Canada. 2016. Available at: http://www.livingin-canada.com/salaries-for-dentists.html.

- Taylor B. Marketing in an audiology practice. San Diego, CA: Plural Publishing; 2015.

- Shargorodsky J, Curhan SG, Curhan GC, Eavey R. Change in prevalence of hearing loss in US adolescents. JAMA 2010;304(7):772–78. doi:10.1001/jama.2010.1124.

- Lin FR, Niparko JK, and Ferrucci L. Hearing loss prevalence in the United States. Arch Intern Med 2011;171(20), 1851–53.

- Windmill IM and Freeman BA. Demand for audiology services: 30-yr projections and impact on academic programs. J Am Acad Audiol 2013;24(5), 407–16.